House flipping is a real estate investment strategy that can lead to amazing returns. However, it comes with risks and requires careful planning. Successful flipping depends on factors like market conditions, property location, renovation costs, carrying costs, and your ability to accurately estimate resale value.

Before starting a flipping venture, investors should perform extensive research, develop a comprehensive budget, and gain a deep understanding of the local real estate market.

This guide is here to help you optimize your fix and flip strategy. Here, you'll find tips to:

- Find the right property to flip

- Analyze your costs and create a budget

- Finance your deal

- Make the best offer on a property

- Keep the transaction on track

- Plan and manage your renovation

- Market and sell your property quickly

Need help funding your flip? Get to the closing table faster with a SkyBeam Capital loan.

Finding the Right Property to Flip

The first step in any successful flip is finding the right property to invest in. Here are some things to keep in mind when searching for a potential flip:

- Location: The old saying "location, location, location" holds true when it comes to house flipping. Look for properties in desirable neighborhoods with good school districts, access to public transportation, and amenities like parks and shopping centers.

- Your Buyer: Think of your buyer before purchasing a flip and ensure the elements of the house you can't change, like location, match your intended audience's desires. First-time homebuyers, high-end buyers, and other investors will have varying expectations, so keep this buyer in mind as you make purchasing and design decisions.

- Your Skill Set: Consider your own skills and experience when searching for a flip. If you have experience in carpentry or construction, you may be able to take on more extensive renovations. But if you're new to flipping, it's best to start with a property that requires only cosmetic improvements.

- Condition: The condition of the property is crucial when choosing a potential flip. Avoid properties with major structural issues or code violations, as these can quickly eat into your budget and delay the selling process.

- Market Conditions: Being attuned to market conditions helps an investor make informed decisions, optimize their investment strategies, and maximize their potential returns. Ignoring factors like employment rates, housing supply, homebuyer demand, interest rates, material and labor costs can lead to extended holding periods, higher carrying costs, and reduced profit margins.

- Price: Set a budget for purchasing the property and stick to it. Look for properties priced below market value, but also make sure there is room for profit after renovation costs.

💡Investor Tip: Focusing on subdivision data is critical when finding the perfect property to flip.

Know the Local Real Estate Market

The real estate market is highly local, often hyperlocal. What holds true in one area may not apply to another. Pay close attention to what comparable homes (comps) sell for in the area before making any offers. This will give you a realistic idea of the profit margins you can anticipate.

Gather information on your local market from platforms like Zillow, Realtor.com, or Redfin. If you don't have a real estate agent license, access comprehensive listings and market states for specific regions on an MLS database by working with a local real estate agent or broker.

Dive deeper into local data with resources like the U.S. Census Bureau, local government websites, and the Federal Housing Finance Agency's price index reports and market analysis. Other real estate market publications to keep an eye on include the National Association of Realtors (NAR), and CoreLogic.

Finally, take some time to explore online data platforms that aggregate data from multiple sources and provide detailed property reports, market analytics, and tools to calculate your return on investment (ROI).

Define Your Buy Box

Once you become more familiar with the real estate market, outline the specific criteria you'll use to determine which properties align with your buyer's needs, your budget, and your investment goals.

This list of criteria, or buy box, usually includes factors like location, property types, price range, condition, square footage, age of the property, zoning, crime rates, and susceptibility to environmental risks.

By defining a buy box, you can quickly filter out properties that do not meet that criteria and focus your efforts on viable investment opportunities. This strategy optimizes the search process and increases efficiency in making investment decisions.

Where to Search for a Property

There are several ways to find your ideal property for a fix-and-flip investment:

- Foreclosures: Properties in foreclosure can offer great deals but come with risks.

- REO (Real Estate Owned) Listings: These are properties owned by lenders (banks, mortgage companies) after an unsuccessful foreclosure auction. Websites like Bank of America’s REO listings, HUD Home Store, and individual bank websites can be helpful.

- Auctions: Properties foreclosed by banks or government agencies often end up at auctions. Websites like Auction.com, RealtyTrac, and local county auction sites are good places to start.

- MLS (Multiple Listing Service): Real estate agents have access to the MLS, which often lists distressed properties. Working with a knowledgeable agent can help you find these listings.

- County Tax Assessor's Office: Properties with delinquent taxes are often a sign of distress. Contacting or checking the website of your local tax assessor can provide leads.

- Driving for Dollars: Physically driving through neighborhoods to spot neglected or abandoned properties and noting down addresses can lead to potential deals.

- Local Courthouse Records: Checking public records at your local courthouse for properties in foreclosure, probate, or bankruptcy can uncover distressed properties.

- Direct Marketing: Sending letters or postcards to owners of vacant or neglected properties, or those in pre-foreclosure, can yield responses from motivated sellers.

- Wholesalers: Real estate wholesalers often have distressed properties under contract. Networking with wholesalers can provide off-market deals.

- Networking: Real estate investment groups, online forums, and social media groups dedicated to real estate investing can be valuable resources for finding distressed properties.

- Online Real Estate Marketplaces: Websites like Zillow, Redfin, and Trulia frequently list foreclosures and pre-foreclosures.

While distressed and foreclosures will often yield a higher return, fix and flip investors should look for properties that offer potential for appreciation from the perspective of the end buyer too. Keep a close eye on market trends to identify areas with rising property values, new businesses, infrastructure projects, and community improvements as these areas will likely to continue to attract and sustain buyer interest.

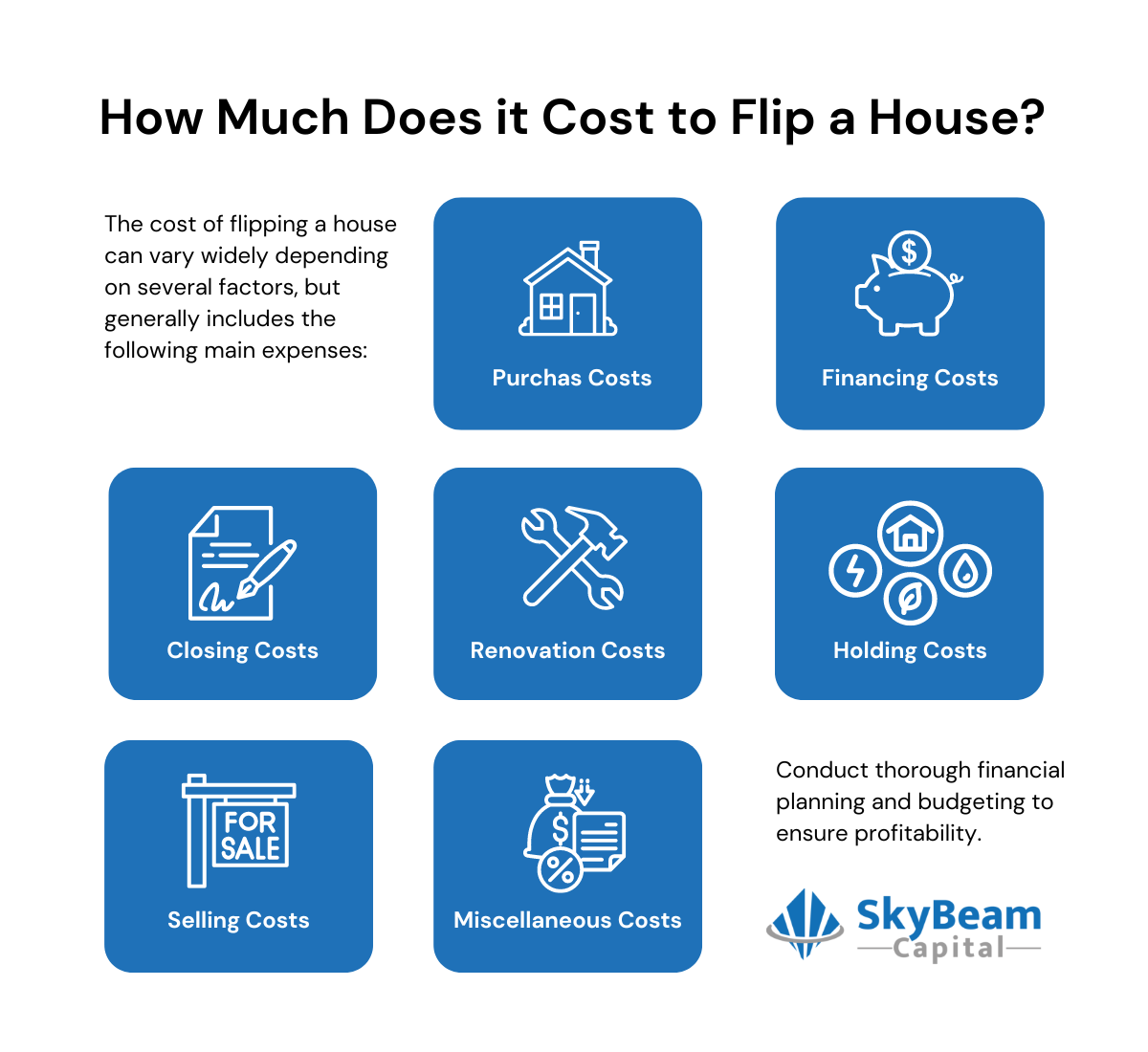

Budgeting For Your Fix and Flip

Budgeting effectively is crucial for a fix-and-flip investor to ensure profitability and mitigate risks. Here’s a detailed breakdown of how to budget when buying a property:

1. Initial Purchase Costs

- Purchase Price: This is the agreed amount to buy the property. Research comparable properties (comps) in the area to ensure you're not overpaying.

- Earnest Money Deposit: Typically 1-2% of the purchase price, put down to show serious intent to buy.

- Down Payment: If financing, this will usually be 20-25% of the purchase price, depending on the lender's requirements.

2. Financing Costs

- Loan Origination Fees: Fees charged by the lender to process your loan, often 1-3% of the loan amount.

- Interest Payments: Calculate based on the expected time frame for the project. Short-term loans or hard money loans typically have higher interest rates.

3. Closing Costs

- Title Insurance: Protects against potential title disputes.

- Attorney Fees: Legal assistance for closing the deal.

- Inspection Fees: Cost for professional inspection to uncover any hidden issues.

- Appraisal Fees: To determine the market value of the property. (if needed)

4. Renovation Costs

- Repair Estimates: Obtain detailed quotes from contractors for all anticipated repairs and upgrades.

- Materials: Budget for the cost of materials needed for renovations.

- Labor: Calculate labor costs based on contractor rates.

- Permits and Fees: Include all necessary permits and fees required for renovation work.

- Contingency Fund: Set aside an additional 10-20% of the renovation budget for unexpected expenses.

5. Holding Costs

- Property Taxes: Estimation based on the property's assessed value.

- Utilities: Monthly costs for water, electricity, gas, etc.

- Insurance: Property insurance during renovation.

- Maintenance: Regular upkeep and minor repairs during the holding period.

- HOA Fees: If applicable, include homeowner association fees.

6. Selling Costs

- Real Estate Agent Commissions: Typically 5-6% of the final sale price.

- Closing Costs: Additional fees associated with selling, such as transfer taxes.

- Staging and Marketing: Costs to professionally stage and market the property.

- Concessions: Potential concessions offered to the buyer, such as covering part of their closing costs.

7. Miscellaneous Costs

- Unexpected Expenses: Budget for contingencies to cover unforeseen issues that may arise during the renovation.

Example Breakdown of How Much It Costs to Fix and Flip

Assume the following figures:

- Purchase Price: $200,000

- Closing Costs: $8,000 (4% of purchase price)

- Loan Origination Fees: $6,000 (3% of loan amount)

- Interest Payments: $12,000 (assuming 1 year at 10% interest on a $120,000 loan)

- Renovation Costs: $50,000

- Contingency Fund: $5,000 (10% of renovation costs)

- Holding Costs: $5,000 (for 6 months)

- Selling Costs: $15,000 (6% real estate commission + additional closing costs)

- Staging and Marketing: $3,000

Total Costs:

[ {Total Costs} = $200,000 + $8,000 + $6,000 + $12,000 + $50,000 + $5,000 + $5,000 + $15,000 + $3,000 = $304,000 ]

In this example, the total cost to flip the house would be approximately $304,000. The actual costs can vary based on specific circumstances, but this breakdown gives a comprehensive view of typical expenses involved in a house flip. Accurate budgeting and cost management are crucial to ensuring profitability in a fix-and-flip venture.

Funding Your Flip

Securing funding before making an offer on a property is crucial for increasing your credibility, expediting the closing process, ensuring accurate budgeting, and gaining a competitive advantage in the market.

There are several options to consider:

Funding Options for House Flippers

- Hard Money: Hard money loans are short-term loans secured by real estate, often used by flippers to finance their projects. These loans are fast and flexible but may come with higher interest rates and fees.

- Cash: If you have the capital, buying with cash can simplify the process and save on interest costs. However, tying up so much capital into one property could reduce your opportunity to make deals on other properties and diversify your portfolio.

- Traditional Bank Loan: Conventional loans can be used for flips but may come with stricter requirements and longer approval processes. Generally, a larger down payment is needed, making this option challenging for investors with limited capital.

- Private Lender: Getting a loan from a private individual like friends, family, and other investors can give you quick access to cash. Approach this funding method with caution because a bad investment could wreck your personal relationship.

There are pros and cons of every funding option. Consider factors like your financial situation, credit history, risk tolerance, timeline, and the specific property when selecting the right funding option for your flip. It is always advisable to consult with a financial advisor or real estate attorney before making any decisions related to financing your flip.

Take your flip to the finish line with a local private lender. Investors throughout the Southeast work with Skybeam Capital to reach their real estate goals. Learn more about our loan programs.

Making the Best Offer on a Property

After securing your funding or pre-approval, prepare for negotiations by conducting thorough subdivision research and property analysis to understand the property's value and necessary repair costs. It's crucial to determine the seller's motivation and tailor your offer to meet their needs. Building rapport with the seller and highlighting your ability to close quickly can strengthen your position. Be prepared to negotiate repair credits and closing costs, and always know your limits to avoid overpaying.

Many investors use a simple calculation called the 70% Rule to help them determine the highest offer they can make and avoid a money pit.

What's the 70% Rule?

The 70% Rule is a commonly used guideline in real estate investing, particularly for fix and flip projects. It helps investors determine the maximum price they should pay for a property to ensure a profitable flip. To calculate the offer price, take 70% of the After Repair Value and subtract the Repair Costs.

- After Repair Value (ARV): The estimated market value of the property after renovations are completed.

- Repair Costs: The total expenses required to renovate the property to reach the ARV.

Formula

[{Maximum Purchase Price} = ({ARV} \times 0.70) - \{Repair Costs} ]

Example Calculation

Let’s assume:

- ARV: $300,000

- Estimated Repair Costs: $50,000

Using the 70% Rule:

[{Maximum Purchase Price} = ($300,000 \times 0.70) - $50,000 ]

[{Maximum Purchase Price} = $210,000 - $50,000 ]

[{Maximum Purchase Price} = $160,000 ]

In this example, an investor should pay no more than $160,000 for the property to ensure a profitable flip, assuming the ARV and repair costs are accurate.

Investor Tip: While this formula can be a useful guide, the 70% Rule may not apply to every fix-and-flip situation. Be sure to take into consideration your risk tolerance and your market's unique characteristics when making an offer.

Keeping the Transaction on Track

Effective communication and organization are key to keeping the transaction on track. Start by assembling a reliable team that includes a real estate agent experienced in investment properties, a trusted contractor, an inspector, and a real estate attorney. Clear communication and regular check-ins with your team can help address any issues promptly and ensure everyone is on the same page.

Home Inspection

Home Inspection

A thorough home inspection is a pivotal step in the fix and flip process, ensuring you are fully informed about the property's condition and potential issues. Hire a qualified home inspector to identify any structural, mechanical, or cosmetic problems that could affect your renovation budget or timeline. During the inspection, focus on key areas such as the foundation, roof, electrical systems, plumbing, and HVAC systems. Ensure that the inspection report is detailed and includes photographs and estimated repair costs for any identified issues.

Check Ownership History and Zoning

Alongside the home inspection, conduct your due diligence to mitigate risks and uncover any hidden problems. This may involve researching the property's title history to ensure there are no liens, easements, or encumbrances that could affect ownership. You should also check local zoning laws and regulations to confirm that your intended renovations and usage are permissible. Additionally, assess neighborhood factors, such as crime rates, school quality, and proximity to amenities, which can influence the property's resale value.

Negotiate Repairs and Concessions

Once you've identified necessary repairs from the home inspection, you can use this information as leverage during negotiations. Start by compiling a list of critical issues that need to be addressed and estimate the costs associated with each repair. Present this information to the seller, and request either a reduction in the purchase price or repair credits to offset these costs. Be prepared for the seller's counter-offer, and remain flexible yet firm on your non-negotiables to ensure the deal remains profitable for you.

Estimating Profits and Setting Timelines

Accurately estimating potential profits and setting realistic timelines is essential for a successful house flip. After receiving the home inspection, recalculate your After Repair Value (ARV) and compare it with similar properties in the area. Analyze recent sales data and current market trends to refine your estimates. From here, prepare a detailed budget that includes all anticipated costs, from acquisition and financing charges to renovation expenses and selling fees.

Finalizing the Purchase

After renegotiating based on the inspection results, it’s essential to move quickly to finalize the purchase. Ensure that all paperwork is complete, and clear any outstanding conditions before the closing date. Work closely with your real estate agent, lender, and attorney to ensure a smooth transaction process. Arrange for the transfer of utilities, and prepare for the renovation phase to commence immediately after the closing. Having a detailed timeline and a reliable contractor lined up will help you stay on track and meet your investment goals.

Renovation Planning and Management

Effective renovation management is key to the success of your fix-and-flip project. Develop a comprehensive renovation plan that outlines all required improvements, budgets, and timelines. Prioritize high-impact renovations that boost the property’s value, such as kitchen and bathroom upgrades, flooring, and curb appeal enhancements.

Download the Rehab Budget Sheet to keep your fix and flip on track

Contractors and Subcontractors

Hiring the right contractors and subcontractors is critical to the success of your renovation. Look for professionals with experience in fix-and-flip projects and check their references and past work. Maintain clear communication with your contractors, regularly visit the site to monitor progress, and address any issues promptly. Keeping the renovation on schedule and within budget is critical to maximizing your return on investment.

Permits and Regulations

Navigating the permit and regulations landscape is an indispensable part of your renovation plan. You must secure all necessary permits before starting any work, as failure to do so can result in fines, penalties, or forced halts in progress. Visit your local building department or municipality's website to understand which permits are required for your specific renovations. Common permits include those for electrical work, plumbing, structural changes, and additions. Ensure your contractors are licensed and familiar with local building codes to streamline the approval process.

Managing Renovation Costs

Staying on top of your renovation budget is crucial for a profitable flip. Create a detailed line-item budget that includes all anticipated costs, and remain vigilant about tracking expenses throughout the project. Utilize real estate investing software tools or spreadsheets for real-time budget monitoring. Be wary of scope creep—additional work or changes that were not part of the original plan—as these can quickly escalate costs. Always have a contingency fund to cover unexpected expenses, typically around 10-20% of your total budget.

Managing Holding Costs

To manage holding costs effectively, minimize the holding period by completing renovations swiftly and efficiently, and choose financing options with favorable terms to reduce interest expenses. Ensure the property has adequate insurance coverage to protect against unforeseen events and keep utility costs low by monitoring usage carefully. Additionally, begin pre-marketing the property before renovations are complete to attract buyers early and facilitate a quick sale.

Marketing and Selling the Flipped Property

Once renovations are complete, it’s time to market the property effectively to attract buyers. Invest in professional photography and staging to highlight the property’s best features. Utilize multiple marketing channels, including online listings, social media, and open houses, to reach a wide audience. Price the property competitively based on a comparative market analysis, and be prepared to negotiate with potential buyers to finalize the sale. Your goal is to sell the property quickly while maximizing your profit.

Marketing the Property

As renovations near completion, begin strategizing the marketing of your property. High-quality photos and videos are essential for showcasing your work—consider hiring a professional photographer. Craft compelling listings that highlight the most attractive features and recent upgrades. Use multiple channels to reach potential buyers, including online real estate platforms, social media, and open houses. Partnering with an experienced real estate agent can also provide valuable insights and expand your reach.

Staging for Sale

Staging the property can significantly impact how potential buyers perceive it. A well-staged home helps buyers visualize themselves living in the space, which can accelerate the selling process and potentially increase the final sale price.

According to the National Association of Realtors, staging the living room was found to be the most important for buyers (39%), followed by the primary bedroom (36%) and kitchen (30%).

Focus on creating inviting, neutral spaces with a few tasteful furnishings and decor pieces. Declutter and depersonalize the space to minimize distractions. Pay attention to curb appeal; a well-maintained exterior will make a strong first impression. Simple touches like fresh paint, new landscaping, and clean windows can make a big difference.

Flipping houses can be a rewarding and profitable venture, but it requires careful planning, strategic execution, and the right team. By following the steps outlined in this guide, you'll be well on your way to becoming a successful real estate investor.

While flipping can yield high returns in a short period of time, investors should be prepared for unexpected challenges and have a contingency plan in place. Diversifying your real estate investment portfolio and considering long-term strategies alongside flipping can help minimize risk and maximize overall profitability.

.webp?width=851&height=771&name=Location%20Guide%20Cover2%20(1).webp)